NCLT Mumbai-V (2024.05.07) in Mr. Vijendra Kumar Jain Vs Mr. Nitin Ramchandra Jadhav and Ors..[(2024) ibclaw.in 515 NCLT, I.A. 677 of 2023 in CP (IB) No. 1023 of 2021] Held that;.

Thus, by taking a cue from the judgments rendered by the English Courts in this regard, the following acts have been held to constitute ‘Wrongful Trading’;

(i) Repaying the director loan made to the company while other creditors were not paid;

(ii) Repayment of a loan to a family member;

(iii) A director paying his own salary while the salary for the employees was not paid;

(iv) Buying goods on credit when there is no means to pay for them;

(v) Using customer deposits for cash-flow purposes with no means of supplying goods;

(vi) Repaying bank personal guarantees over other creditors;

(vii) Not keeping proper accounting records;

(viii) Falsification of company records; and

(ix) Any transfer or sale of assets at anything less than a fair and reasonable commercial value.

Excerpts of the order;

# 1. The present application bearing I.A. No.677 of 2023 is filed by the Resolution Professional of the Corporate Debtor, Mr. Vijendra Kumar Jain (hereinafter referred to as the “Applicant”) seeking direction against the suspended board of directors, namely, 1) Mr. Nitin Ramchandra Jadhav, 2) Mr. Bhavrao RamKrishna More and 3) Mr. Amol Jadhav (hereinafter referred to as the “Respondents”) under Section 66 of the Insolvency and Bankruptcy Code, 2016 (hereinafter called as “the Code”) praying for following reliefs:-

“..this Hon'ble Tribunal be pleased to:-

a. Pass appropriate Orders/Directions declaring that the transaction enumerated in this application is fraudulent trading/ wrongful trading in terms of Section 66 of the IBC;

b. Pass appropriate Orders/Directions against the Respondent to make contribution of Rs.9,04,61,725/- or more to the Corporate Debtor;

c. Pass order/directions for further investigation of Enforcement/Investigation Agencies of the transaction highlighted by the Transaction Auditor;

d. Pass appropriate Orders/Directions to allow the newly appointed liquidator Mr. Ram Sethia to take over the present application (if required so) as and when appropriate Orders to the Application u/s 33 of the Code is allowed by this Tribunal;

e. And pass any such other order(s) as this Hon’ble Adjudicating Authority may deem fit and proper in the interest of justice”.

BRIEF FACTS OF THE CASE:

# 3. In the Second CoC meeting dated 03.09.2022, the COC appointed Mr. Parekh Shah & Lodha as the Forensic Auditor to carry out the transaction audit of the books of account of the Corporate Debtor for the last 5 years. However, in the Third CoC meeting dated 29.09.2022, the CoC noted that the suspended directors had failed to furnish the Audited Financials and Tally Back-up of Accounts of the Corporate Debtor for financial years 2017-18 to 2021-22 and for the broken period from 01.04.2022 to 20.07.2022 along with certain other documents and details as sought by the Resolution Professional and the Forensic Auditor. In these circumstances, the Resolution Professional filed an interlocutory application bearing I.A. No.3392 of 2022 under Section 19(2) of the Code before this Tribunal on account of the non-cooperation of the management which is pending adjudication.

# 4. Further, in the Third CoC meeting, it was noted that the Corporate Debtor i.e. Gajanan Solvex Limited, had made an investment of Rs.8,84,91,725/ - in its subsidiary Company by and under the name of M/s. Rio Resource PTE. Ltd. which is a Singapore branch of the Corporate Debtor. This Company (M/s. Rio Resource PTE. Ltd.) had Fixed Deposit of 3 (Three) Million USD with the Indian Bank, Singapore Branch. Thereafter, it was further informed to the CoC that the Indian Bank had filed an Application against one M/s. Gajanan Oil Private Limited (which had availed the credit facility by creating a lien on the above fixed deposit) before the Hon’ble High Court, Bombay praying for injunction from presenting the Fixed Deposit receipt for discharge. The Hon’ble High Court, Bombay allowed the ad-interim injunction on the reasoning that the bank had extended the Credit Facility against the said fixed deposit. However, Mr. Nitin Jadhav the suspended director of the Corporate Debtor apprised the CoC that there was no lien on the Fixed Deposit and the same was still intact with the Indian Bank, Singapore Branch.

# 5. In the Fourth CoC meeting held on 28.10.2022, the Chairman/Resolution Professional informed that in view of no progress in the transaction audit report and lack of efforts on part of the then Forensic Auditor and considering that the time-bound process of CIRP was getting hindered, it had been decided to appoint one Shambhu Gupta & Co. as Forensic Auditor to conduct the Forensic Audit of the Corporate Debtor.

# 6. Thereafter, in the Fifth CoC meeting dated 08.12.2022, the CoC was presented with the Dun and Bradstreet Credit Report (hereinafter referred as ‘DNB Report’) of the Subsidiary Company i.e. Rio Resources PTE Ltd. It was apprised that as on date, no shares of M/s. Rio Resource PTE Ltd were held by M/s. Gajanan Solvex Ltd i.e., the Corporate Debtor and instead, 100% shareholding of M/s Rio Resource PTE Ltd. was held by one M/s. Bellwether International Trade PTE Ltd. The name of M/s. Rio Resource PTE Ltd was changed to Aspira Co. PTE Ltd and Mr. Amogh Malviya and Mr. Chee Teng Joo were its new directors with effect from June, 2022. However, the audited financials of the Corporate Debtor as on 31.03.2022 still showed investment of Rs.8,84,91,725/- in M/s.Rio Resource PTE Ltd. whereas, as per the DNB Report, these shares had been transferred on 20.02.2019 and no consideration for the same had been received by the Corporate Debtor.

# 7. The Forensic Auditor also recorded a finding pertaining to M/s. Rio Resource PTE Ltd. The Auditor mentions that as on 23.06.2017, 19,00,000 shares of M/s. Rio Resource PTE Ltd. were allotted to the Corporate Debtor for Rs.8.85 crores. After such investment, the Corporate Debtor held 51% shares in M/s. Rio Resource PTE Ltd. which thus became a subsidiary of the Corporate Debtor. When explanation was sought by the Resolution Professional, the suspended management stated that on 20.02.2019, the Corporate Debtor had transferred the said 19,00,000 shares to Mr. Amogh Malviya and Mr. Chee Teng Joo, directors of M/s. Bellwether International Trade PTE Ltd. However, perusal of Books of Account of the Corporate Debtor for financial year 2021-22 clearly and categorically reflected investment of Rs.8,84,91,725/- in the shares of M/s. Rio Resource PTE Ltd. under the head “Investments in the subsidiary”.

# 8. Subsequently, the Resolution Professional sent multiple reminders to the suspended board of directors enquiring about the consideration received on transfer of shares held by the Corporate Debtor in Rio Resource PTE Limited. The Corporate Debtor vide its email dated 12.01.2023 came up with a contract with one Aero Steel Resources Ltd., UAE and a share transfer agreement with Bellwether International Trade PTE Ltd., according to which the Corporate Debtor had sold its shares in M/s. Rio Resource PTE Ltd to M/s. Bellwether International Trade PTE Ltd. However, as per the audited balance sheet of the Corporate Debtor for the Financial Year 2021-22, the Corporate Debtor still holds the investment in M/s. Rio Resource PTE Ltd.

# 9. It is submitted by the Ld. Counsel for the Applicant that as per the DNB Report of Aspira Co. PTE Ltd. (previously known as M/s. Rio Resource PTE Ltd.) as on 23.11.2022, the net worth of the Company was Rs.282 Crores while perusal of the share transfer agreement showed that the shares were purportedly transferred for a consideration of approximately Rs.19.95 Crores which is 3.45% of the net worth of M/s. Rio Resource PTE Ltd. This clearly indicates that the Corporate Debtor had sold shares of its subsidiary M/s. Rio Resource PTE Ltd. to Bellwether International PTE Ltd. at a loss after its loan accounts with the Financial Creditor were declared NPA in April, 2018. This fact itself is unacceptable, strange and against the prudent business sense. When the same was questioned, the Corporate Debtor claimed that a penalty of 1.8 million USD under a contract with Aero Steel Resources Ltd. was settled against payment of 1.37 Million USD by Bellwether International PTE Ltd. However, as per RBI guidelines, settling of inflow balance of one foreign company with outflow balance of another foreign company is prohibited. Therefore, the payment to Aero Steel Resources Ltd. by Bellwether International Trade PTE Ltd. on account of the Corporate Debtor was, in fact, an illegal and unjustifiable act.

# 10. It is further submitted that on perusal of the sales invoices of the Corporate Debtor which were received for inspection, the vehicle numbers specified in these invoices were not found on Vahan.com which gives rise to suspicion about the genuine nature of the transactions. Pursuant to transaction audit, it was concluded that the said sales invoices were fraudulently created in order to show fictitious sales. The Forensic Auditor observed that the transportation proofs were also not made available in all cases and upon enquiry with transporters, it was discovered that no transaction of transport ever took place with HMD Transporter Co. and Sai Kripa Transporter. It was noted that the alleged transporter, Sai Kripa Transporter was actually a farmer by profession.

# 11. The Forensic Auditor also noted that the Corporate Debtor had purportedly shown to have made transactions approximately amounting to Rs.282.56 crores with certain firms/ entities owned by individuals who were the ex-employees of the Group Companies i.e., Mr. Subodh Ingale of M/s. Shakti Trading/ Shakti Soya Industries, Mr. Sachin Adsul of M/s. Varun Agro Traders and Mr. Udhay Kishan Deepak Vyas of M/s. Shri Tirupati Traders.

# 12. Further, the Forensic Auditor also observed that the Corporate Debtor had purchased goods from M/s. Shakti Soya Industries for Rs.84,00,00,000/-. However, as per the GST Website, the GST registration of M/s Shakti Soya Industries was cancelled suo motu effective from 31.12.2017 but as per the books of account of the Corporate Debtor, GST was levied on purchase of goods from M/s. Shakti Soya Industries even after the cancellation of the said registration. The Forensic Auditor also observed that the Corporate Debtor had shown to have sold goods worth Rs.134.42 crores to M/s. Shri Tirupati Traders which was owned by one Mr. Deepak Vyas who was the employee of one of the group companies of the Corporate Debtor. The Forensic Auditor also noted that Inventory was brought down from Rs.51.69 crores in the financial year 2017-18 to about Rs.72 lakhs in the financial year 2018-19. Likewise, Sales were shown at only Rs.63.76 crores in the financial year 2018-19 as against Rs.450 crores in the financial year 2017- 18. In this regard, the suspended board of directors replied that they were unable to explain reasons for cancellation of GST registration by respective department. They claimed that this fact had been suppressed by respective supplier and was not known to the Respondents at the time of making transactions. In view of above findings of forensic audit, it is prayed that the Respondents be directed to make appropriate contribution to the Corporate Debtor for their acts of fraudulent/ wrongful trading in terms of Section 66 of the Code.

# 13. The Forensic Auditor while analysing various sales done by the Corporate Debtor observed that the Corporate Debtor had made a sale of Rs.19,70,000/- to M/s. SR Minerals. However, on scrutiny, it was found that no such party existed in the books of account of the Corporate Debtor.

# 14. The CoC in its Sixth meeting held on 23.12.2022 approved the Resolution for filing the Liquidation Application under Section 33 of the Code with 80.46% voting. Accordingly, IA No.310 of 2023 was filed by the Resolution Professional which was pending adjudication wherein Mr. Ram Sethia is proposed to be the Liquidator. The said application was reserved for orders on 30.01.2023. Thus, in the present Application, it is prayed that as and when the said Liquidation Application is allowed and the proposed Liquidator Mr. Ram Sethia is appointed as Liquidator, the present Resolution Professional be discharged and replaced by the Liquidator, Mr. Ram Sethia.

REPLY OF THE RESPONDENTS

# 15. The Learned Counsel for the Respondents has filed the affidavit-in reply dated 23.08.2023 and denied all the allegations and averments contained in the Application.

# 16. It is submitted that the Accounting and Corporate Regulatory Authority (ACRA) is equivalent to the Registrar of Companies (RoC) or MCA in India, where all companies incorporated in Singapore have to compulsorily file all their annual reports, shareholding, etc. As per the filings of Rio Resources PTE. Ltd. available on ACRA website, the company, Rio Resources PTE. Ltd. got incorporated on 29.06.2015. At that time, the company had a share capital of 37,21,000 Singapore dollars divided into 3721000 shares of 1 dollar each. The shareholders at that time were (i) Gajanan Solvex Limited (the Corporate Debtor herein) having 19,00,000 shares and (ii) Pillai Nand Kumar having 18,21,000 shares. Hence, Rio Resources PTE. Ltd. was a subsidiary of Corporate Debtor at that time. It is further submitted that, as per the filing available on ACRA website as on 01.02.2019, the Corporate Debtor still held 19,00,000 shares . But, as per the Report filed by Rio Resources PTE. Ltd. as on 19.02.2019, Gajanan Solvex Limited’s holding became zero and only Bellwether International Trade PTE. Ltd. was appearing as the shareholder of Rio Resources PTE. Ltd. This clearly reveals that all the shares held by Corporate Debtor in Rio Resources PTE. Ltd. got transferred in the month of February, 2019 during the period from 01.02.2019 to 18.02.2019. Therefore, the contention of the Applicant that the said transaction pertaining to transfer of shares after the commencement of CIRP is an afterthought is baseless and false.

# 17. It is further submitted that the Income Tax Department conducted search operation on Gajanan Solvex Limited during 21.08.2018 to 26.08.2018 wherein officials of the I.T. Department had seized all the documents, books of account, Tally data, hard disk, server and other records of Gajanan Solvex Limited. The same is well reflected in their Panchnama dated 23.08.2018. The GST search operation was also conducted on 21.12.2018 wherein all documents pertaining to sale and purchase of goods, invoices, challans, etc. were confiscated. As regards the transaction of sale of goods worth Rs.19,70,000/- to M/s. SR Minerals, it is claimed that no such party existed in the books of account of the Corporate Debtor because the sale made was cancelled. It is contended that this cannot be considered a fraudulent transaction solely on this basis.

# 18. With regard to the contention of the Applicant that despite transfer of shares of M/s. Rio Resources PTE Ltd. by the Corporate Debtor on 20.02.2019, its audited financials as on 31.03.2022 and books of account for financial year 2021-22 still reflected the above investment, the Respondents submitted that they were unable to give proper information about investment to the accountant and, therefore, the accountant had carried it over from previous year. Hence, the company auditor had also taken this investment in the audited financial statements. It was further submitted that the Respondents were under pressure from the CoC to get the books of account audited as early as possible. Hence, due to lack of evidence, the auditor had not squared off or made any changes to the financial statement of Financial Year 2021-22 related to this transaction. Therefore, it was admitted that the audited books of account wrongly show the investment in Rio Resources PTE Ltd. in the audited financial statements of Financial Year 2021-22. But it was pointed out that the same had been changed in the provisional financial statement for Financial Year 2022-23 up to 20.07.2022 and sent to the Resolution Professional.

# 19. As regards the contention of the Applicant that the Corporate Debtor had sold the shares of its subsidiary company i.e. M/s. Rio Resource PTE Ltd. at a loss, it was submitted that the shares were transferred for a consideration of Rs.19.95 crores approximately. It was pointed out that the Corporate Debtor had sold the shares on 20.02.2019 whereas the DNB report showed the net worth of the company as on 23.11.2022. The Respondent thus argued that valuing the shares sold in 2019 on the basis of 2022 report would not be proper.

# 20. With regard to the transaction with Aero Steel Resources Ltd., Dubai, the Respondent submitted that the Corporate Debtor had entered into an export contract with Aero Steel Resources Ltd. to deliver a quantity of 1,00,000 Metric Tonnes (MT) of Soya DOC (De Oiled Cake) at the rate of 360 USD per metric ton within a contract period of 12 months vide Contract No.GSL/EXPO/01/2017 dated 15.10.2017. The total contract thus amounted to USD 36 million. As per the said contract, if the Corporate Debtor failed to supply the commodity as agreed, the seller would compensate the buyer maximum up to 5% of the Contract value. The condition of breach of contract is reproduced below:-

"Breach of Contract: In case, if seller failed to supply/ deliver the commodity as agreed in this contract within the delivery period, then seller agrees to compensate due to non-supply of material which is maximum up to 5% of the contract value."

# 21. The Respondents claimed that the Corporate Debtor had failed to perform the contract and, consequently, Aero Steel Resources Ltd. had executed the condition for breach of contract wherein the seller/Corporate Debtor had to compensate the buyer for maximum up to 5% of the contract value which worked out to 18,00,000 USD. However, it was contended that the Corporate Debtor had settled the matter at 13,70,000 USD by selling its investment in RIO Resources PTE Ltd., Singapore to Bellwether International Trade PTE Ltd., Singapore vide Shares Purchase Agreement dated 31.12.2018 and paying the said compensation to Aero Steel Resources Limited, Dubai. It was submitted that Aero Steel Resources Limited vide letter dated 21.01.2019 had confirmed to have received the said compensation from Bellwether International Trade PTE Ltd., Singapore on behalf of the Corporate Debtor. It was pointed out that the same had been incorporated in the provisional financial statement prepared as on 20.07.2022.

# 22. Finally, with respect to the RBI guidelines prohibiting settlement of inflow balance of one foreign company with outflow balance of another foreign company, the Respondent submitted that to avoid any legal actions with respect to Aero Steel Resources Limited in foreign courts, the Respondents had not gone for any valuation at the time of adjusting the penalty to be paid for the breach of contract. The Respondents argued that the Corporate Debtor had to settle at a loss. It was contended that they were not setting off the inflow balance with the outflow balance as they were to receive the money in their account, instead they instructed Bellwether International Trade PTE Ltd. to give the money to the Aero Steel Resources Limited. Therefore, it was claimed that there was no violation of RBI guidelines.

FINDINGS

# 23. Heard the Ld. counsels and perused the entire record with their able assistance.

# 24. From the perusal of records, it is revealed that the present Application is filed by the Resolution Professional under Section 66 of the Insolvency and Bankruptcy Code, 2016 against the Respondents i.e., the suspended board of directors of the Corporate Debtor based on the findings of the transaction audit report of the Forensic Auditor, M/s. Shambhu Gupta & Co.

# 25. At the outset, we deem it appropriate to appreciate the provisions of Section 66 of IBC which is reproduced as under: - . . . . . . . .

# 26. A careful perusal of Section 66 of IBC, 2016 reveals that it deals with two types of transactions: Section 66(1) of IBC, 2016 deals with ‘Fraudulent Trading’ and Section 66(2) of IBC, 2016 deals with ‘Wrongful Trading’. Section 66(1) of IBC, 2016 imposes liability to make contribution to the assets of the Corporate Debtor on ‘any persons’ who were knowingly parties to the carrying on of the business with a dishonest intention to defraud the creditors. Thus, essentially for a transaction to qualify under Section 66(1) of IBC, 2016, the following conditions should be satisfied:-

(a) Liability can be fixed upon ‘any person’ including but not limited to the Directors;

(b) Such business of the Corporate Debtor undergoing insolvency has been carried on with a dishonest intention to defraud the creditors or for any other fraudulent purpose; and

(c) The said persons have participated in the carrying on of business of the Corporate Debtor knowingly i.e., with the knowledge that the transactions they were participating in were intended to defraud the creditors of the company or were in some other way fraudulent. All the above ingredients are required to be fulfilled so as to make a transaction fall under Section 66(1) of the IBC.

# 27. As far as Section 66(2) is concerned, following ingredients must be satisfied before invoking the charge of ‘wrongful trading’:-

a) The act in question has taken place before the insolvency commencement date.

b) The directors of the Corporate debtor knew or ought to have known that there was no reasonable prospect of avoiding the commencement of CIRP.

c) The directors did not exercise the due diligence in minimising the potential loss to the creditors of the Corporate Debtor.

d) A director of the Corporate Debtor shall be deemed to have exercised due diligence, if such diligence was reasonably expected of a person carrying out the same functions as are carried out by such Director in relation to the Corporate Debtor.

# 28. It thus emerges that the definition of ‘Wrongful Trading’ in Section 66(2) does not clearly delineate as to which act committed by a Director of the Company would amount to 'Wrongful Trading'. It is pertinent to mention that the concept of 'Wrongful Trading' has been imported from the UK Insolvency Act, 1986 into the IBC, 2016 which is still at a nascent stage in this country. Thus, by taking a cue from the judgments rendered by the English Courts in this regard, the following acts have been held to constitute ‘Wrongful Trading’;

(i) Repaying the director loan made to the company while other creditors were not paid;

(ii) Repayment of a loan to a family member;

(iii) A director paying his own salary while the salary for the employees was not paid;

(iv) Buying goods on credit when there is no means to pay for them;

(v) Using customer deposits for cash-flow purposes with no means of supplying goods;

(vi) Repaying bank personal guarantees over other creditors;

(vii) Not keeping proper accounting records;

(viii) Falsification of company records; and

(ix) Any transfer or sale of assets at anything less than a fair and reasonable commercial value.

# 29. Let us now consider whether the present Application filed by the Resolution Professional/ Applicant makes out a good and sufficient case of fraudulent trading/ wrongful trading against the Respondents. In this connection, it would be pertinent to refer to the primary facts relevant to the issue at hand. It is observed from the record that at the request of the Corporate Debtor, the Financial Creditor (State Bank of India) sanctioned a Fund Based Working Capital (FBWC) limit of Rs.20 Crores and a Fund Based Term Loan (FBTL) limit of Rs.35 Crores inclusive of a Letter of Credit (LC) limit of Rs.1.25 crores under a Letter of Arrangement dated 03.11.2011. Thereafter, the credit facilities were enhanced and renewed under Letters of Arrangement dated 21.03.2013, 16.03.2015 and 02.03.2017. The Corporate Debtor confirmed the balances in the loan accounts and executed a Balance Confirmation Letter dated 31.03.2017 for Rs.32,32,32,793/- in the Cash Credit Facility and Rs.15,54,37,181/- in the Term Loan Facility.

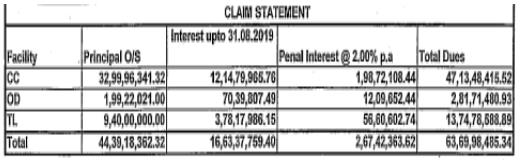

# 30. However, a default took place on part of the Corporate Debtor in January, 2018. The Financial Creditor requested the Corporate Debtor to pay off the amount due in the loan accounts. The Financial Creditor declared the loan accounts as NPA in April, 2018. Despite several requests made by the Financial Creditor, the Corporate Debtor failed to clear its dues. Thus, on account of nonpayment of outstanding dues, the Financial Creditor issued notice under Sections 13(2) of SARFAESI Act, 2002 on 29.08.2018. The requisite Form 1 under the head “Particulars of Financial Debt” contains the following particulars of computation of amount claimed to be in default:-

# 31. After hearing both the parties and upon perusal of the application and Section 66 of the Code, this Bench observes that the forensic audit report issued by the M/s. Shambhu Gupta & Co. wherein the auditor under the head ‘Analysis of Subsidiary of Corporate Debtor’ had reported that

“1. As per ABS of FY 2021-22; Corporate Debtor was having investments in Rio Resource Pte. Ltd. Suddenly as on 06th Jan 2023 corporate debtor claimed that these investments were sold as on 31st December 2018 but these investments were continued in the balance sheet of CD; this indicates that corporate debtor has either misreported or was veiling such transactions from its bankers which comes under Fraudulent Transactions as specified U/Sec.66 of IBC, 2016 .

2. As per terms of Contract with Aerosteel Resources Limited; there would be liability of 5% of the contract value in case of inability to fulfil the terms of contract but no such information was disclosed in the Audited Balance sheet for FY 2017-18.

Inference –

Based on our review and reply received from management of the Rio Resource Pte. Ltd. and unusual indicators mentioned above, Amount of Rs. 8.85 crores shown as investment in the ABS of the Corporate Debtor will fall under Section 66 of the IBC, 2016.”

After having appreciated the facts that the inference carried out by the Forensic auditor in his report, no credible evidence has been produced by the Respondents/ directors so as to counter the finding of the Forensic auditor. In view of the peculiar facts and circumstances of the present case we are left with no other option but to endorse the findings of the forensic auditor.

# 32. For proper appreciation of the transactions highlighted by the Applicant, the following chart deserves to be taken note of:

Gajanan Solvex Limited (Corporate Debtor) entered into an agreement with Aerosteel Resources Limited of UAE, wherein Gajanan Solvex Limited (Corporate Debtor) to provide Soya DOC quantity of 100000 Metric Ton (MT) valuing to USD 36 Million to Aerosteel Resources Limited however Gajanan Solvex Limited failed to provide Soya DOC as per the agreement. Thereafter, Gajanan Solvex Limited (Corporate Debtor) transferred shares of its subsidiary Company, Rio Resources PTE Ltd. (later known as Aspira Co. PTE. Ltd.) to Bellwether International PTE Ltd on 31.12.2018 at 1.37 Million USD. Further, Bellwether International PTE. Ltd. on behalf of Gajanan Solvex Limited (Corporate Debtor) has paid 1.37 million USD to Aerosteel Resources Limited of UAE for settlement of penalty for breach of contract by Gajanan Solvex Limited (Corporate Debtor) with Aerosteel Resources Limited of UAE amounting to 1.8 million USD.

# 33. The main contention of the Applicant is that perusal of the books of account of the Corporate Debtor reflects different picture from the facts stated by the Suspended Directors of the Corporate Debtor i.e., the Respondents. In view of the same, the Respondent during the course of arguments has submitted that there was a search operation by the Income Tax Department on Gajanan Solvex Limited conducted during 21.08.2018 to 26.08.2018 and GST search operation on 21.12.2018. The I.T. Department’s officials had confiscated all the documents, books of account, Tally data, hard disk, server and other records of the Corporate Debtor i.e., Gajanan Solvex Limited during the said search. The same is well reflected in their Panchnama dated 23.08.2018. The contention of the Corporate Debtor further is that the GST officials had also taken away all documents pertaining to sale and purchase of goods, invoices, challans etc. Therefore, the Corporate Debtor could not draw its annual accounts and as a consequence, there was no audit or annual report or balance sheet during the period 2018 to 2022. However, this Bench is of the view that the submissions made by the Corporate Debtor in its defence are nothing more than a frivolous and futile attempt to cover up their own lapses as the Income Tax Department and also GST at the time of search operation carry only back-up copies of data stored in computers etc. and later grant due opportunity to the searched entities/ persons to get photo-copies of all the documents required by them during the course of their business. Therefore, the contention of the Respondents on this count does not survive.

# 34. It is also observed by this Bench that the Respondents/Suspended Directors from the year 2018-2022 (five years) have not paid any heed to the collection of information for the preparation of books of account of the Corporate debtor but suddenly in the year 2023 after facing the pressure from the CoC, the Respondents/Suspended directors prepared the Financial statements for the last 5 years in just 3 days which shows that the Respondents were in possession of the complete data /back-up of the entire records or accounts statements which is further corroborated from the fact that on the intervention of the CoC, the Respondents managed to submit the record within a period of 3 days. Thus, the submission of the Respondents that the entire record was not available with them is falsified with their own conduct and this further proves that there was an attempt to supress the relevant documents from the other stakeholders including the creditors of the company.

# 35. While appreciating the facts of the present case, the Forensic Auditor while elaborating a finding pertaining to M/s. Rio Resource PTE Ltd., mentions that as on 23.06.2017, 19,00,000 shares of M/s. Rio Resource PTE Ltd were allotted to Corporate Debtor for Rs.8.85 Crores. After such investment the Corporate Debtor held 51% shares in M/s. Rio Resource PTE Ltd. which basically became a subsidiary of the Corporate Debtor. When explanation was sought by the Resolution Professional, the Suspended management stated that on 20.02.2019 the Corporate Debtor transferred the said 19,00,000 shares to Mr. Amogh Malviya & Mr. Chee Teng Joo directors of M/s. Bellwether International Trade PTE Ltd. However, the Books of Accounts clearly reflect under the head “Investments in the subsidiary” an investment of Rs.8,84,91,725/- existing in the M/s. Rio Resource PTE Ltd. Therefore, it is evident that the Respondents/Suspended Directors are guilty of falsification of the records of the company.

# 36. It is an admitted fact that the Corporate Debtor transferred all the 19,00,000 shares held in the subsidiary company i.e., M/s. Rio Resource PTE. Ltd. during the month of February, 2019 which was much before the insolvency commencement date but after the issuance of SARFAESI Notice under section 13(2) on 29.08.2018 for a consideration of Rs.19.95 crores approximately on 20.02.2019 whereas as per the DNB report, the net worth of the Company was stated to be Rs.282 crores. In response to the contention of the RP, the Corporate Debtor has taken the plea that valuing the shares of Rio Resource sold in 2019 and valuing the same on the basis of DNB Report of 23.11.2022 is not proper and hence the transaction cannot be said to be a fraudulent transaction. The onus to prove the correctness of the transaction was on the Corporate Debtor which the Corporate Debtor has miserably failed to discharge by neither placing on record the Valuation Report of 2019 nor of the year 2022. Thus on the basis of the bald statement, the onus on the Corporate Debtor does not get discharged. The Corporate Debtor has failed to place on record any credible documentary evidence like financial statements of Rio Resource PTE. Ltd. for relevant period, net worth statement or valuation report of shares from a registered valuer etc. in order to demonstrate that the price at which the shares of M/s. Rio Resource PTE. Ltd. were sold in February, 2019 represented the fair market value of such shares. Thus it is evident that the said transaction is to the detriment of the creditors of the Corporate Debtor.

# 37. The directors of the Corporate Debtor knew or ought to have known that the Financial Creditor had already initiated action under SARFAESI Act for enforcement of security interest by issuing notice under Section 13(2) on 29.08.2018. The Corporate Debtor had failed to discharge their liabilities to the Financial Creditor within the stipulated period. Further, there was no reasonable prospect of avoiding the commencement of a CIRP in respect of the Corporate Debtor. In these circumstances, the directors of the Corporate Debtor had a statutory obligation to exercise due diligence with a view to minimise the potential loss to the creditors of the Corporate Debtor which they failed to discharge in the present case. In the peculiar facts and circumstances of this case, a heavy onus lies on the directors so as to prove that the said sale of shares of M/s. Rio Resource PTE. Ltd. at a loss was not an exercise in ‘asset stripping’ intended to take the Corporate Debtor’s assets beyond the reach of the creditors.

# 38. It is generally understood that the primary duty of directors is towards the shareholders. The provisions of ‘wrongful trading’ u/s 66(2) of IBC modifies this position and the focus of the directors shifts away from shareholders towards creditors of the company once it enters the twilight zone of insolvency. As per the report of the Bankruptcy Law Reform Committee (which was instrumental in drafting the IBC), the objective behind introducing the provision of ‘wrongful trading’ under IBC was to accord protection to creditors who may suffer from information asymmetry while dealing with a distressed company.

# 39. The present case is not one of mere failure to exercise due diligence in order to minimise potential loss to creditors of the Corporate Debtor but is a case of gross and wilful failure coupled with an unabashed falsification of books of account of the Corporate Debtor so as to avoid easy detection. This is evident from the fact that having sold the shares of Rio resource in February, 2019 itself, the Directors of the Corporate Debtor did not disclose this transaction in the books of account/annual financial statements of F.Y. 2018- 19 onwards. Such suppression and misrepresentation of transaction of Sale of shares of Rio Resource continued even in subsequent Financial Years 2019-20 and 2020-21 which amounts to suppression of facts with a view to mislead and defraud the creditors of the Corporate Debtor. According to the Applicant, the Corporate Debtor is shown to be holding investment is shares of M/s. Rio Resource PTE. Ltd. even in the balance sheet for F.Y. 2021-22. The directors of the Corporate Debtor admit in the reply that necessary changes in this regard have now been made in the provisional financial statement for F.Y. 2022-23.

# 40. It deserves to be noted that merely incorporating transactions pertaining to F.Y. 2018-19 in the provisional financial statement for F.Y. 2022-23 is of no consequence and is legally impermissible, because the profit earned on sale of investment in foreign subsidiary was required to be disclosed in the books of account as well as income-tax returns of the Corporate Debtor for A.Y.2019- 20. It is also admitted that the Respondents were unable to give the proper information about investment in M/s. Rio Resource PTE. Ltd. to the accountant and the company auditor. This evidently brings out that the whole transaction was carried out by the Respondents in a clandestine manner so as to defraud the creditors of the Corporate Debtor. Thus, it clearly emerges that there was a conscious and deliberate attempt on part of the Directors/Respondents at falsification of books of account of the Corporate Debtor so as to hide their blatant act of ‘wrongful trading’ within the meaning of Section 66(2) of the IBC. Instead of exercising due diligence in minimising and mitigating the potential loss to the creditors of the Corporate Debtor, we find that the Directors /Respondents were actively engaged in ‘wrongful trading’ and indulging in desperate practices such as ‘asset stripping’ to the sheer detriment of the interests of creditors of the CD. Thus from the perusal of the above it is evident that the conduct of the Respondents/directors of Corporate Debtor clearly falls within the framework of ‘wrongful trading’.

# 41. The manipulative tale of ‘wrongful trading’ does not end with mere sale of shares of M/s. Rio Resource PTE. Ltd. The next step in this ‘wrongful trading’ was to keep the sale proceeds of shares of subsidiary company ‘M/s. Rio Resource PTE. Ltd.’ out of the kitty of the CD and far away from the reach of the creditors of the CD. With this end in view, an agreement is shown to have been reached with Aero Steel Resources, UAE. The transaction on behalf of Respondent by Bellwether International Trade PTE Ltd. to Aero Steel Resources Ltd. was never brought on record but was stated for the first time after the admission of the Corporate Debtor into CIRP. Keeping in view the conduct of the Respondents/Directors and the manner in which the attempt has been made to not only supress the actual facts but also reflect the factually incorrect record in the books of account to their knowledge leaves us with the suspicion that the entire transaction with respect to the Aero Steel Resources Ltd. is also a façade so as to take away the funds from the Corporate Debtor to the detriment of the Creditors and also against the guidelines of RBI. Liquidator is further directed to look into the violation of the provisions of FEMA by way of nonrepatriation of sales proceeds of shares by the Corporate Debtor. It is highly intriguing to note that the Respondents/Suspended Board of Directors who have been vehemently opposing the CIRP proceedings of the Corporate Debtor and not extending any cooperation at all to the RP in discharge of his functions and obligations under the IBC could not export the ordered quantity or even part thereof over a period of 12 months and meekly, readily 8 and willingly agreed to pay liquidated damages of huge amount to Aero Steel Resources Ltd. on a platter without raising any objection or invoking clause 10 (Force Majeure) or Clause 12 (Arbitration). It is equally baffling to find that on the one hand, the Corporate Debtor claims that it failed to perform the contract “due to financial crunches” and on the other hand, it agreed to supply goods worth 36 million USDs or over Rs.200 crores at the relevant time without insisting on any advance payment or Letter of Credit (LC) against future supplies. The Corporate Debtor has not produced any documentary evidence to show that Aero Steel Resources Ltd. had invoked the ‘breach of contract’ clause. Obviously, such a transaction could by no stretch of imagination be said to have been entered in the ordinary course of business of the Corporate Debtor. We are of the considered opinion that the issues regarding the transactions with Aero Steel Resources Ltd. deserve to be further enquired into /investigated by SFIO. In addition, strangely, the Corporate Debtor before making the payment of 1.37 USD Million to Aero Steel Resources Ltd. failed to place on record sufficient material so as to justify the payment of the said amount by keeping the Creditors in dark.

# 42. Finally, even with regard to sales of Rs.19,70,000/- made to M/s. SR Minerals, the respondents have not been able to furnish credible evidence to substantiate their claim that the above sales were cancelled. In view of the above facts, the Bench is of the considered view that the aforesaid transactions reflect the nature of being fraudulent and also wrongful trading as per Section 66 on the part of the Respondents who are held guilty under Section 66 of IBC.

# 43. Accordingly, the present I.A. is allowed. The Respondents are held liable to make contributions towards the assets of the Corporate Debtor under Section 66(1) and also under Section 66(2) of the Insolvency and Bankruptcy Code, 2016. The Respondents are directed to contribute the amount of Rs.9,04,61,725/- as calculated below to the assets of the Corporate Debtor within a period of 30 days from the date of receipt of certified copy of the order:-

Further, as the sale proceeds of shares were not repatriated to the account of the Corporate Debtor in India, the Respondents are directed to make additional contributions on account of Profit earned on the sale of the shares of Rio Resources PTE Ltd. As stated above, the said shares were bought in the year 2017 for a consideration of Rs.8.85 crores and sold in 2019 for a consideration of Rs.19.95 Crores. Therefore, the profit on sale of said shares needs to be deposited into the account of the Corporate Debtor. The Liquidator is directed to calculate the profit realised on transfer of shares, intimate the same to the Respondents/ suspended directors and ensure that such amount of profit is deposited in the account of the Corporate Debtor within a period of 30 days from the date of receipt of certified copy of the order. The liability for making aforesaid contributions to the assets of the Corporate Debtor is jointly as well as severally of the Respondent/ suspended directors of the Corporate Debtor. The matter is directed to be further investigated by SFIO. The copy of this order be forwarded to the SFIO for the necessary compliance. The compliance of this order be reported back by the SFIO and also the Liquidator i.e. Mr. Ram Sethia after a period of 60 days from the date of receipt of certified copy of this order. Resolution Professional i.e. Mr. Vijendra Kumar Jain be treated as having being discharged from this assignment.

-------------------------------------------

No comments:

Post a Comment